Strategic Decision Framework

I led a comprehensive analysis of two placement options, evaluating multiple dimensions including technical complexity, revenue impact, user experience, and ownership autonomy.

The Two Options

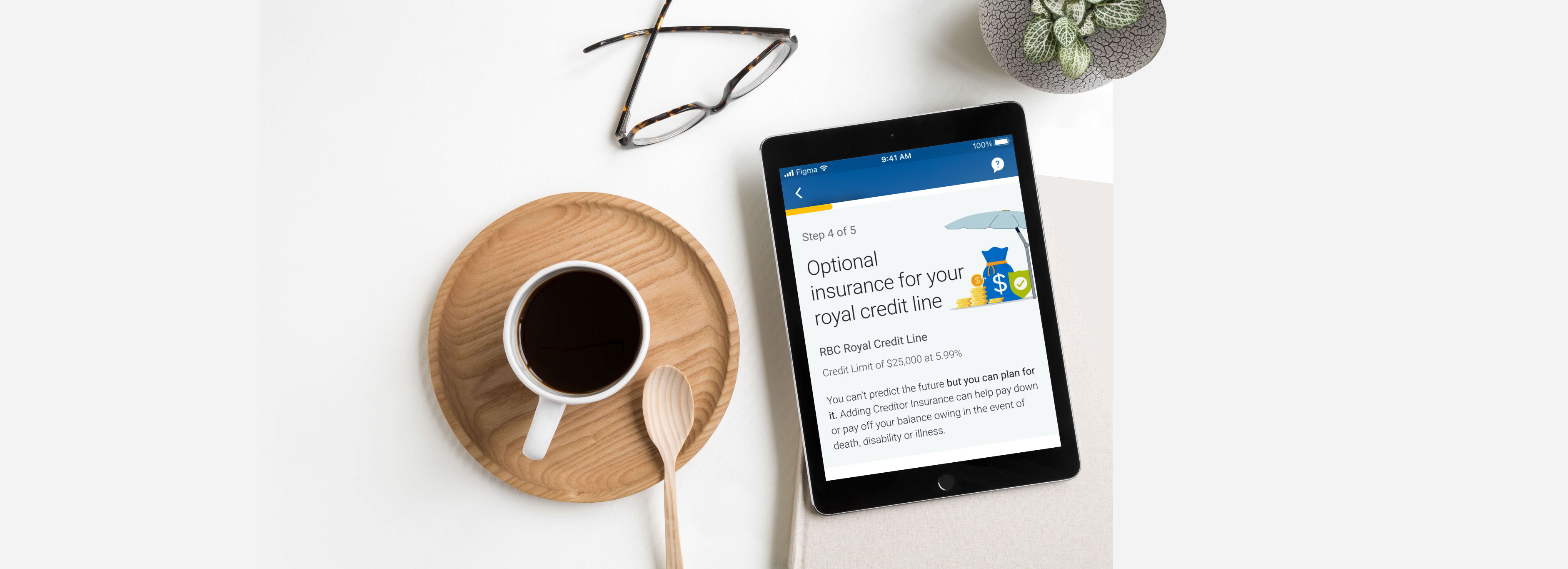

Inflow Widget (During Banking Activation)

- Technical Complexity: Moderate—required shared screens implementation

- Revenue Impact: Faster uptake—users encounter insurance during active engagement

- User Experience: Seamless—insurance feels like natural part of the process

- Ownership: Partial—some screens shared with Banking

- Integration: Complex—shared screens and content management

Post-Activation Flow (After Banking Completion)

- Technical Complexity: Lower—standalone widget with single handoff

- Revenue Impact: Potentially lower—risk of drop-off after primary task completion

- User Experience: Seamless but separate—clear division between Banking and Insurance

- Ownership: Full—Insurance owns all steps independently

- Integration: Straightforward—single handoff point

Decision: Inflow Widget Approach

Despite the moderate technical complexity, I recommended and successfully advocated for the inflow widget approach. This strategic decision prioritized revenue optimization and user experience over technical simplicity.

Key Rationale:

- Revenue Optimization: Capturing users during active Banking engagement would deliver significantly higher conversion rates than post-activation approaches, where drop-off was a significant risk

- User Experience Excellence: Insurance would feel like a natural extension of the Banking process rather than an afterthought, increasing perceived relevance

- Strategic Timing: Users were most receptive to additional financial products during their primary Banking task, not after completion

- Manageable Trade-offs: The technical complexity could be addressed through careful shared screen architecture

graph LR

subgraph "Decision Factors"

A[Technical

Complexity] --> D{Inflow

Widget}

B[Revenue

Impact] --> D

C[User

Experience] --> D

D --> E[Selected

Approach]

end

style A fill:#e67e22

style B fill:#27ae60

style C fill:#27ae60

style D fill:#3498db

style E fill:#2ecc71

Inflow Integration Architecture

.jpg)

.jpg)